Finance for a greater good? According to BloombergNEF data, sustainable debt issuance surpassed USD 1 trillion in 2019. Green bonds continue to hold center stage, but proposed EU regulations and rapid market developments are expected to have an impact.

This article is part of SANDS’ series on Sustainable Finance and aims to give an overview of some legal aspects of bonds used as tools towards a low-carbon economy (“green bonds”). We will also draw some parallels to bonds earmarked for wider sustainability purposes, like social and gender equality (“social bonds”).

Green Bonds – main characteristics

Green bonds are bonds whose proceeds are used to fund environment-friendly projects. In the Green Bond Principles (further described below) such projects are referred to as “Green Projects”.

Green Projects are typically projects related to renewable energy, energy efficiency, sustainable water and wastewater management, pollution prevention, green buildings and other projects with a positive environmental impact. As further described below, green bonds can also capture activities whereby issuers transition into more sustainable activities.

Green bonds can be linked to the underlying green activity in various ways, including:

- Financing greenfield development;

- Asset acquisition financing;

- Refinancing existing projects; or

- “Pure play” green bonds (by issuers that earn all or most of their revenues from green activities), with no defined link between the bond proceeds and a specific project

Issuers of green bonds range from sovereigns (national governments) and sub-nationals (provinces, cities or sub-national governmental agencies), to financial and non-financial corporates.

A green bond can be structured in different ways, the most common types [1] being:

- Standard Green Use of Proceeds Bond

- A standard debt obligation with recourse to the issuer;

Green Revenue Bond - A non-recourse debt obligation in which the credit exposure in the bond is to the pledged cash flows of the revenue streams, fees, taxes etc., and whose use of proceeds go to related or unrelated Green Project(s);

- Green Project Bond

- A project bond for one or more Green Project(s) for which the investor has direct exposure to the risk of the project(s), with or without potential recourse to the issuer; and

Green Securitised Bond - A bond collateralized by one or more specific Green Project(s) including but not limited to covered bonds, ABS, MBS, and other structures. The first source of repayment is generally the cash flows of the assets.

- More creative structures may also be available, for instance bonds with land lease like features for the purpose of conserving or re-establishing land areas in their natural state to protect endangered nature and wildlife (“eden bonds”) [2].

Legal framework today and coming EU regulations

There is currently no Norwegian legislation directed at green bonds or social bonds as such. Such bonds will, as transferable financial securities, similarly to any other bonds, be subject to applicable laws and regulations on securities issuance and securities trading [3]. For a green bond, its sustainability features could qualify as non-financial information that is comprised by mandatory disclosure requirements under the applicable prospectus requirements, as such information may be considered necessary for the investor to make a properly informed assessment. Listed green bonds may similarly be subject to ongoing disclosure obligations related to reporting on the relevant project or activity, which could include non-financial information linked to its environmental benefits.

The proposed EU regulations under the Sustainable Finance Action Plan will not be directly applicable to green bonds or green loans. However, the newly developed voluntary EU Green Bond Standard (see section below) will require that the EU Taxonomy is used for a bond to be marketed as s EU Green Bond. The proposed enhanced disclosure regulations related to sustainability aspects of financial instruments will also be linked to the EU Taxonomy, but as currently proposed on a “comply or explain”-basis. Further, a financial product may only be EU eco-labelled if the Taxonomy is used for assessing its greenness. EUs work on sustainable finance have largely been tilted towards the environmental aspect of sustainability, and financial instruments for other or wider ESG purposes, like social bonds, have so far not been addressed specifically under the action plan.

Notwithstanding the lack of clear legal regulation on ESG-financing, market practice for green bonds (and social bonds) has been developing over several years based on various initiatives from key market players, with standards, principles and guidelines that are largely being followed.

Why are green bonds attractive?

Green bonds are the most mature instrument in the sustainable debt market. Since the launch of the first green bond in 2007, Bloomberg data as of October 2019 show that USD 788 billion of green bonds have been issued in total, and that green bonds and green loans issuance for 2019 alone exceed USD 200 billion.

In addition to the intrinsic value of contributing to sustainable activities, and thereby promoting the issuer’s environmental profile, green bonds have the potential benefit of reaching a broader investor base. The global shift towards greener finance makes more capital available for sustainable activities, which may also positively affect pricing of green bonds versus traditional bonds. It is however debated whether there is sufficient grounds to state that a “greenium” (more favourable pricing due to the environmentally positive profile) applies in general to green bonds. Apart from a few local initiatives, there are at the moment a lack of clear tax incentivisation for sustainability linked bonds. Neither do sustainable financial products currently enjoy benefits of more favorable risk weighting, however that is being investigated as part of the EU Action Plan.

Are green bonds just for green businesses?

No. Green bonds are available in various forms, and in short it is the project or purpose for which the proceeds are to be used that determines eligibility.

While the product may have traditionally been utilized by issuers within sectors that typically are perceived as green or sustainable, like the renewable energy sector, several green bonds have also been issued by companies that operate in “high carbon” markets like transportation and fossile energy.

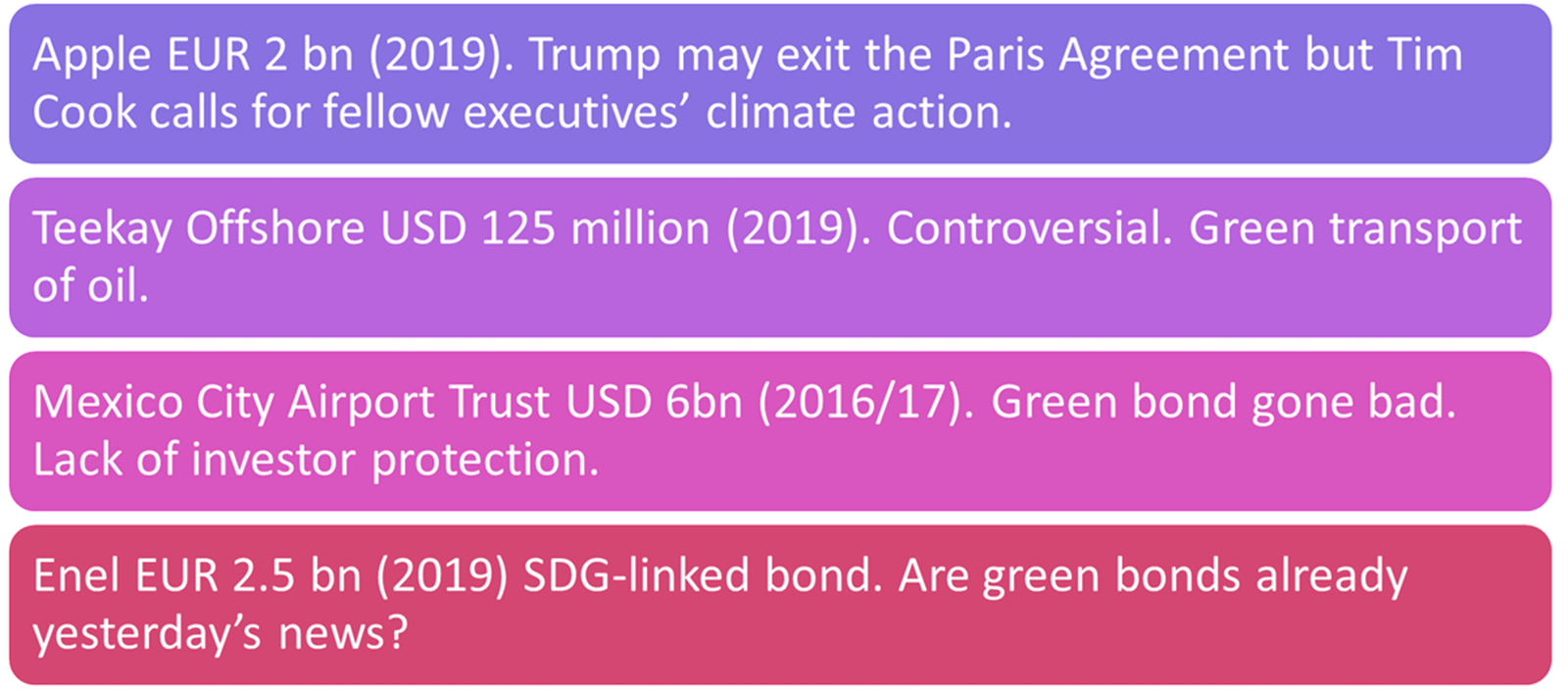

To illustrate, earlier this year the Norwegian hydropower company Småkraft AS issued an EUR 50 million bond, rated dark green by Cicero. NorgesGruppen, a Norwegian grocery wholesaling group issued a NOK 400 million green bond to finance clean transportation, green buildings and renewable energy, which was also labelled dark green. And in October this year, the oil transportation company Teekay Offshore issued a USD125 million bond to finance more environmentally friendly shuttle tankers, a bond which Cicero rated light green.

Bonds from which the proceeds are earmarked to projects which will help a company shift to more sustainable operations are also regularly referred to as “transition bonds”.

Green Listing – what is required?

In January 2015, Oslo Stock Exchange became the first stock exchange in the world with an exclusive list for green bonds; “the Green List”. Since launch, a steady stream of interested borrowers have gathered sizable sums through issuances of green bonds - as of June 2019 there were 27 green bonds listed with an outstanding amount of NOK 28.6 billion, and the number of green bonds have since reached 32. The list comprise bonds listed both on the Oslo Stock Exchange and on the Nordic ABM [4].

In addition to ordinary listing requirements, to be listed on the Green List a bond must be accompanied by an independent third-party evaluation. Further, reporting requirements agreed with the bondholders related to the environmental aspect of the bond must be publicly disclosed to the market.

To increase exposure and visibility of the loan as an environment-friendly investment, green bonds have the suffix G in the ticker symbol.

How is “green” determined?

Market standard principles and guidelines

Numerous standards, guidelines and principles have been developed based on various initiatives, and there is currently not one globally recognized methodology for determining what is “green”. The Green Bond Principles of the International Capital Market Association [5], which currently has over 300 members and observers [6], is however widely recognized in the market, and do to a large extent form the basis of EU’s work in developing the EU Green Bond Standard.

- The Green Bond Principles have four core components:

- The use of proceeds for Green Projects that provide clear environmental benefits which will be assessed and, where feasible, quantified by the issuer.

- A process for project evaluation and selection that ensures that the Green Projects, their compatibility with environmental sustainability objectives and the potential environmental and social risks are clearly communicated to the investors.

- Transparent management of proceeds, for instance by earmarked “green accounts”, ideally supplemented by the use of an independent auditor.

- Continuous reporting on the use of proceeds and material project developments.

Transparency and continuous reporting (including impact reporting) [7] is of high priority, in particular with regards to ensuring the funds are actually put to use to facilitate progress towards overarching sustainability goals. This is of fundamental importance to maintain the integrity of Green Bond issuances as tools towards a low-carbon economy.

Third party opinions, ratings and indices

To ensure the integrity of green bonds and their compatibility with global environmental objectives, the bond should additionally be assessed and approved by an independent third-party. The third-party assessment seeks to confirm the environmental benefits of the project financed by the bond, and is often carried out pursuant to internationally approved standards such as the Green Bond Principles. Providers of such second opinions for green bonds in the current market include Cicero, Sustainalytics, Vigeo, ISS-Oekom, KPMG and others. Some third party verifiers like Cicero have also developed a classification system whereby the bonds they assess are rated in three shades of green, from light to dark [8]. The darkest green would be the ones with clear environmental benefits and few environmental concerns, like wind energy projects with a strong governance structure. Medium green would for instance be used for bridging technologies like plug-in hybrid buses, whereas the light green shade is projects or activities that are climate friendly but do not contribute long term to climate goals, for instance emissions reduction activities in traditional fossil fuel sectors.

Rating agencies have also developed various frameworks to help financial market participants determine the “greenness” of a project linked to a financial product. A number of green bond indices have also been launched, for instance by Standard & Poor’s, MSCI, and Bank of America Merrill Lynch.

The problem is nevertheless that issuers, arrangers, opinion providers, rating agencies, index administrators and stock exchanges all use overlapping, but not identical, criteria for eligibility, benchmarking and reporting. This lack of comparable data makes the green bond market less effective and transparent, with a risk of “greenwashing”. In an effort to address these challenges, create consistency and encourage the market participants to issue and invest in EU green bonds, a proposal for an EU Green Bond Standard has been developed.

The EU Green Bond Standard

As the green bond markets continue to develop, determining a common language for what is “green” becomes a task of utmost importance to maintain the integrity and credibility of these lending mechanisms’ compatibility with SDG’s and the goals of the Paris Agreement, and to avoid “greenwashing”. The lack of a common classification system and framework for what is “sustainable” or “green” is currently one of the biggest challenges sustainable finance initiatives are facing on a global scale. For green bonds, this problem largely relates to establishing predictable criteria and metrics for the financed Green Projects, that can be used collectively by investors, issuers and third-party verifiers alike.

As part of the EU Sustainable Finance Initiative, a Technical Expert Group (“TEG”) of the EU was set up to draft a proposal for an “EU Green Bond Standard” – a voluntary, non-legislative standard based on best market practice developed to encourage green investments. The EU Green Bond Standard will incorporate the four main components of the Green Bond Principles as listed above.

The EU Green Bonds Standard will also be closely linked to the EU taxonomy, which is being developed based on a separate proposed regulation. The EU taxonomy aims to establish such a common “green language” classification system, by listing a number of economic activities and relevant screening criteria that meet certain sustainability objectives based on scientific data and industry experience. Read more about the EU taxonomy in our previous newsletters.

In the proposal for an EU Green Bond Standard of June 2019, a centralized accreditation scheme for third-party verifiers was presented [9], suggesting an accreditation regime for authorization and supervision by the European Securities and Markets Authority (“ESMA”) implemented through a legislative framework. Having a single competent body for the authorization of third-party verifiers would be an important step towards harmonized supervision across the EU member states.

Furthermore, the TEG elaborates on possible incentives to enhance the growth of green bond issuance. Amongst others, it is proposed to provide financial incentives to support the EU Green Bond market, and to encouraging banks to find ways to enhance pricing of green assets. The proposals include suggestions such as the disclosure of EU Green Bond holdings by European institutional investors and subsidizing – fully or in part – the additional cost associated with external verification. While more complex to implement on an EU wide level, the TEG have also looked into the potential of tax incentives for EU green bonds.

In nature, most green withers. Can a green bond turn brown?

What if the sustainable element of a bond fails, proves to be incorrect, or the project is never completed? The level of investor protection in “green default” situations often depends on the agreed terms and remedies of the bond, which have in many cases been rather limited. That could in certain situations leave the bondholders in a difficult situation. The fact that third parties (rating agencies and or second opinion providers) may in such “green default” situations withdraw their sustainability ratings or opinions, can make the situation for the bondholders even worse.

Not uncommonly, failure to use the proceeds for the intended green or social purposes will not be an event of default which gives the bondholders a right of early termination and repayment. However, several other mechanisms in a bond agreement could be used to create some safeguards relating to the sustainable element of the underlying project. A pricing ratchet linked to certain project milestones or sustainability verifications could to a certain extent mitigate risk where the underlying green project does not develop as initially forecasted to the bond investors. Such a “green grid” mechanism could also be coupled with call options in case of non-compliance with the use of proceeds undertaking, as well as with other specified ESG-related undertakings, to protect the bondholders’ exposure.

Green bond Christmas cocktail conversations?

If you have read your way down here, you will have plenty to contribute with in the conversations. Our guess is that some green bond issuances will continue to be representative of discussion topics while regulators struggle to keep up with market developments and requirements.

Footnotes:

[1] Norway contributes to deforestation and wildlife preservation through several actions and initiatives. Although an “eden bond” structure may still be on the drawing board, several innovative Norwegian green financing initiatives have been launched. In September 2019, a USD 150 million 10-year agreement with Gabon was announced, whereby Gabon will receive payments from Norway for preserving and managing its natural forests, which covers close to 90% of the country. Source: www.cafi.org

[2] In Norway, the Securities Trading Act implements EU requirements on transparency and disclosure under the Prospectus Directive, MiFID II, Regulation (EU) No 60/2014 (MiFIR) and Regulation (EU) No 596/2014 (Market Abuse Regulation).

[3]https://www.oslobors.no/ob_eng/markedsaktivitet/#/

list/bonds/quotelist/ob/OBG/false

[4]https://www.icmagroup.org/green-social-and-sustainability-bonds/green-bond-principles-gbp/

[5]https://www.icmagroup.org/green-social-and-sustainability-bonds/membership/

[6]As an example, ICMA has produced a separate reporting framework for the renewable energy and energy efficiency sectors.

[7]https://www.cicero.oslo.no/en/posts/single/cicero-shades-of-green

[8]https://ec.europa.eu/info/sites/info/files/

business_economy_euro/banking_and_finance/

documents/190618-sustainable-finance-teg-report-green-bond-standard_en.pdf