Responsible Investment

ESG investment strategies are already an integral part of many institutional investors’ and asset managers’ operations. However, the lack of commonly accepted analytical methods for ESG considerations continue to represent a risk to investors. To avoid “greenwashing” and further facilitate sustainable finance, a set of new legal obligations is being developed.

In this brief we look at EU’s proposed legislative measure regarding institutional investors and asset managers’ duties related to sustainability disclosure.

Background

Three new regulations have been proposed as part of the EU Action Plan on Sustainable Finance:

- A regulation to require additional disclosures by asset managers of their approach to ESG and the impacts of their investments on society (the “Sustainability Disclosure Regulation”);

- A regulation to establish a “taxonomy” or classification system for determining whether an economic activity is environmentally sustainable; and

- A regulation to establish low-carbon benchmarks.

It is also proposed complementing specific amendments to the Markets in Financial Instruments Directive II (“MiFID II”) and the Insurance Distribution Directive. [1]

The new disclosure requirements will be supplementary to existing regulatory reporting requirements contained in the Undertakings for Collective Investments in Transferable Securities Directive (“UCITS") and the Alternative Investment Fund Managers Directive (“AIFMD”).

What is the essence of the new obligations?

The proposed new regulation introduces legal transparency obligations for all institutional investors and intermediaries regarding sustainability risks and impacts of their investments.

The proposed regulation will require that all professional or institutional investors make information publicly available as to whether and how they take economic, social and governance (“ESG”) factors and ESG risks into account, and if not, why they do not do so.

The current proposals sets out requirements for ESG-related disclosures and procedures rather than requirements for investments in specified “sustainable” activities.

Is the new Sustainability Disclosure Regulation relevant to me?

The proposed new regulation will apply to a wide group of managers and investment firms, including UCITS management companies, AIFMs, and EuSEF and EuVECA managers. It also applies to banks, where banks conduct investment management on behalf of others.

What are the new disclosure obligations in respect of ESG?

Under the proposed new regulation, the following information must be provided before a contract is entered into with a client:

- Which procedures and conditions are being used to integrate sustainability risks in investment decisions;

- If and how risks related to sustainability are expected to affect the returns of the investment;

- How the firms or managers own remuneration policies relate to the integration of sustainability risks and (where applicable) with the ESG target of the relevant financial product

In relation to MIFID II, the proposed changes means that MIFID II investment firms will have to

- Have (and be able to demonstrate that they have), adequate policies and procedures to ensure that they:

- understand the nature and features (including costs and risks) of investment services and financial instruments selected for their clients, including any environmental, social and governance considerations; and

- assess, while taking into account cost and complexity, whether equivalent investment services or financial instruments can meet their client's profile, including any environmental, social and governance considerations. - Ask whether clients or potential clients are interested in investing sustainably and explain what the options are, for instance by introducing questions in their suitability assessment to identify the client’s preferences regarding environmental, social and governance considerations investment (in addition to the client’s investment objectives and risk tolerance);

- Provide clients or potential clients with (in advance of the provision of investment services or ancillary services) a general description of the nature and risks of financial instruments, taking into account in particular any ESG considerations;

- Make investment recommendations that reflect not only the client’s financial objectives but also any specific ESG preferences of that client, based on a case-by-case analysis;

- Provide the client with information about the types of financial instrument that may be included in the client portfolio and types of transaction that may be carried out in such instruments, including an explanation on how the client’s ESG preferences are taken into account in the process of selecting financial instruments for the client’s portfolio; and

- When providing investment advice to a retail client, the report provided to the client (which includes an outline of the advice given and explains how the recommendation provided is suitable for the client) shall explain how the recommendation meets the client’s ESG preferences as well as its other objectives, (and personal circumstances with reference to the investment term required, the client’s knowledge and experience, and the client’s attitude to risk and capacity for loss).

All information provided in relation to investment and advisory services needs to clear and understandable for investors, and shall be up-to-date, fair, easily accessible and not misleading.

Will there be stricter requirements for so-called “sustainable” investments?

Yes. When professional investors and financial advisors market, contract or report on financial products, such as investment funds, that have as its target sustainable investments, enhanced transparency obligations will apply.

If the product has designated an index as a reference benchmark, it must be disclosed

- how the index is aligned to the sustainability objective of the investment, and

- why it differs from a broad market index.

If the product has carbon emissions reductions as its target, it must be disclosed

- the targeted low carbon emission exposure, and

- (unless a EU low carbon benchmark or positive carbon benchmark is used), a detailed explanation of how the continued efforts of reaching the target is ensured.

For each such financial product the investors have to disclose in their periodic reports [2] methodologies used to assess, monitor and measure the environmental and/or social characteristics, or the impact of the relevant sustainable investment.

Further, within a transition period (to be determined) after the entry into force of the proposed regulation, each financial product shall be coupled with a clear and reasoned explanation of

- whether that financial product considers principal adverse effects of sustainability factors, and if so, an explanation of how, or

- why the financial product does not consider such adverse effects.

More detailed rules about such disclosure obligations is expected to be developed for the relevant sectors.

The EU Taxonomy will in this respect be applicable to investors and advisors on a “comply or explain”-basis.

Scroll down to find the relevant EU definitions for “sustainable investments” and sustainability risks”.

Information to be available online

Investors, financial advisors and providers of investment-based insurance products shall publish on their webpages:

- a written policy on how sustainability is integrated in their investment advice, insurance advise and/or investment decision making processes;

- information on their targets for sustainable investments and the methodology used to measure how the product is sustainable;

- Whether they consider adverse impacts of investment decisions on sustainability factors and,

- if they do, information regarding principal adverse sustainability impact, how such adverse impact is identified and prioritized, and what actions are planned or taken in respect thereof, or

- if they do not, a statement that they do not perform such considerations, their reasons for not doing so, and whether or not they intend to do so; and - information on how their remuneration policies relate to the integration of sustainability risks.

What is meant by “sustainable investments” and “sustainability risks”?

The relevant EU definitions are the following:

“Sustainable investments” mean any of the following or a combination of any of the following:

(i) investments in an economic activity that contributes to an environmental objective, including an environmentally sustainable investment as defined in Article 2 of the Taxonomy Regulation;

(ii) investments in an economic activity that contributes to a social objective, and in particular an investment that contributes to tackling inequality, an investment fostering social cohersion, social integration and labour relations, or an investment in human capital or economically or socially disadvantaged communities;

provided that the investments do not significantly harm any of those objectives and the investee companies follow good governance practices, in particular with respect to sound management structures, employee relations, remuneration of relevant staff and tax compliance.

“Sustainability risk” is defined as an ESG event or condition that could cause an actual or potential negative impact on the value of the investment arising from an adverse sustainability impact.

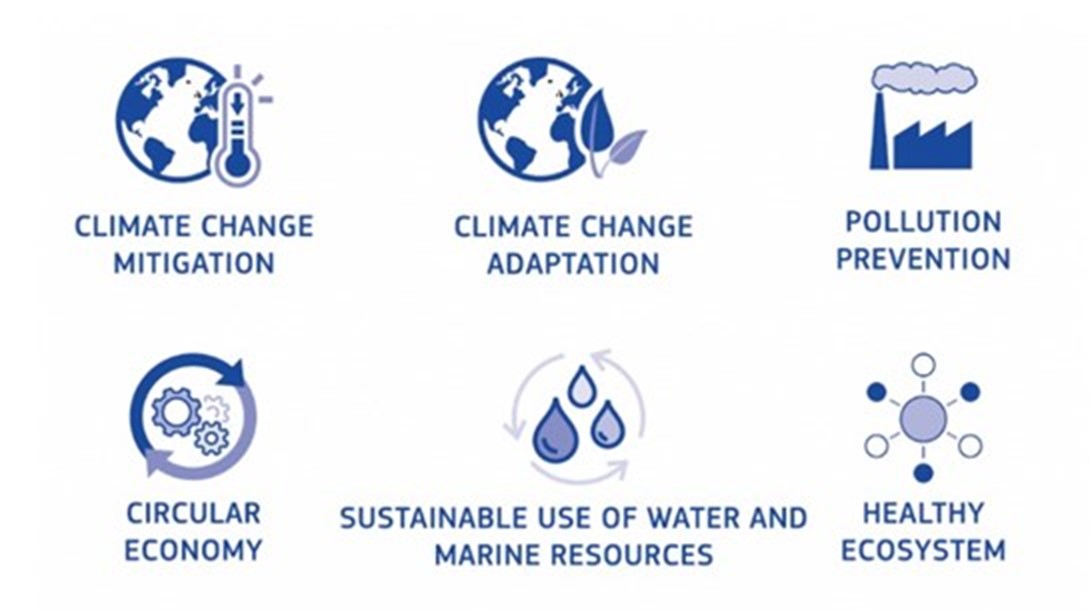

Refresh my memory – what are the environmental EU objectives again?

Enough words. Let’s make it visual

When will the new requirements come into force?

For the private funds industry, the proposed Sustainability Disclosure Regulation may represent the most important legislative change under the EU Action Plan. The EU’s three law-making institutions reached political agreement on the proposal in April 2019, and the new rules are expected to be effective in early 2021.

However it is still debated, even within the European Council itself, what qualifies as “green investment”, for instance in nuclear energy. As the European Council also wants to delay the Taxonomy Regulation until the end of 2022, it may be expected that the Sustainability Disclosure Regulation will also have to be postponed accordingly, as the two are in many aspects interlinked.

The proposed regulations are, once effective, expected to be implemented in Norwegian law through separate legislation or amendments to existing laws.

[1] Regulations that require amendments are the UCITS Directive 2009/65/EC, the AIFM Directive 2011/61/EU, the MiFID II Directive 2014/65/EU, the Solvency II Directive 2009/138/EC and the IDD Directive 2016/97.

[2] For AIFMs, EuVECA and EUSEF managers, their annual reports. For UCITS management companies, their semi-annual and annual reports. For MIFID II investment firms, their periodical reports.